Pakistan's Economy Opportunities and Challenges

I have been asked to speak today on the subject of Opportunities and Challenges for Pakistan's Economy. I have a very simple take on this. The current economic situation definitely presents some opportunities for Pakistan. But the country also has some serious long term challenges. Unless the longer term challenges are decisively tackled, such opportunities will only lead to episodic bursts of growth rather than a sustained upward climb.

Let me start by discussing some opportunities. I see these as arising from five recent developments.

First, low oil prices. Oil prices have been low for over two years now. They have hovered around $50 per barrel over this period after having averaged over $100 between 2010 and 2014. This has been good for the Pakistani economy. It has created much of the fiscal space needed by government to meet the fiscal consolidation targets set by the IMF after 2013 without having to do what previous governments have failed to do, namely, raise domestic revenues by expanding the tax base. It has also given the urban consumer a break since petrol is an important item in his budget. It has kept energy prices in check and thus given industrial consumers a break as well. Oil prices are expected to stay at relatively low levels for the next few years so this opportunity will continue for a while.

Some analysts note that when oil prices decline, remittances decline as well. We have so far been fortunate in this respect. Over the last two years, remittances have not declined. They have kept rising and are currently in the neighborhood of $20 billion per annum. What has however happened is that the rate of growth of remittances has slowed down.

Second, the improved energy situation and outlook. The supply of power to industrial and residential consumers has improved over the past three years. Outages and load shedding have been reduced. The greater supply and predictability of supply to industrial consumers has helped raise industrial production. With new power plants likely to become operational in 2018 and beyond, the supply outlook is favorable. Now it is true that the distributional network has not expanded as needed and the circular debt problem has not been fully resolved but the outlook is still better than it was a few years ago.

Third, the improved security situation and outlook. The number and ferocity of terrorist incidents has declined in recent years. More importantly from the perspective of business, kidnapping and robberies have declined as well. It is also possible that extortion has declined although it is difficult to establish this point empirically.

Fourth, the stabilized economy. The above factors together with disciplined government economic policy have helped stabilize the economy. Compared to 2012-13, the macroeconomic situation is much better. Inflation has declined, international reserves have risen, and the fiscal deficit has come down. For the first time in more than two decades, Pakistan completed a three-year IMF program successfully. Pakistan's credit ratings have improved allowing it to access international capital markets on better terms. The stock market is at an all-time high. Economic growth has averaged 4% over the past three years, up a few basis points from the average rate for the three years prior.

Fifth, CPEC. CPEC refers to the package of energy and infrastructure investments being carried out in Pakistan with the technical and financial help of China. Whatever one thinks of the terms at which this help is being provided, the short term impact is bound to be positive. As much as $50 billion of such investment is planned over the next ten to fifteen years. Such a large injection of investment should result in employment and growth gains.

Long-term challenges

Now we come to the challenges. Despite the improved short term situation several longer term challenges remain. These will continue to exercise a restraint on long term trend growth which, for Pakistan, has been around 4% or so in the last two decades, much below what is needed to absorb new entrants to the labor force at a decent wage and much below the pace attained by regional comparators.

What are these longer-term challenges? There are different ways of describing these. I will use the standard framework employed by academic economists to discuss long term growth. This focuses attention on three main determinants: physical capital, human capital and institutions. Let us take each one of these determinants in turn for Pakistan.

Investment

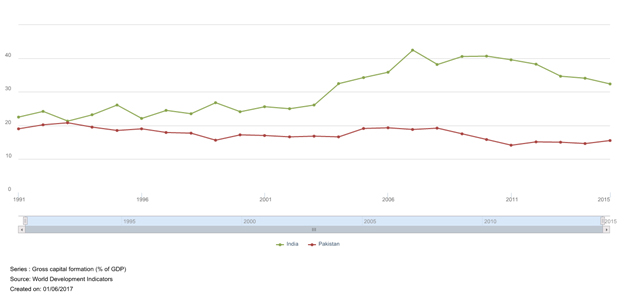

The investment rate in Pakistan has stayed below 20% of GDP since 1991 and has fluctuated around 15% over the last ten years. In recent years, public investment has been around 4% and private investment around 11% of GDP. Both rates are too low to sustain the growth trajectory that Pakistan needs to solve its employment and poverty challenges.

How do these rates compare with the example of the high growth countries of East Asia? In those countries investment rates were typically between 30 and 35% of GDP. In recent years, this has also been the case with our fast-growing neighbor, India. Over the past twenty-five years or so, the total investment rate in India has averaged around 34%. It has varied from a low of 22% in the early 1990s to high of 42% in the mid-2000s. Such investment rates have supported India's impressive growth performance in recent decades just as they did for East Asian countries in earlier decades. Both private and public investment rates in India are much higher than in Pakistan, the former being around 24% currently and the latter around 8%, roughly double that in Pakistan.

What do low private investment rates signify? They signify that, despite the occasional bursts of GDP growth in the economy, private investors are not convinced that the underlying fundamentals are strong enough to justify making long term investments. This is why, despite the soaring stock market, very few IPOs are being launched.

Low private investment rates also signify that private investors are unable to connect to global markets at a large scale. The existing export sectors are not growing much and new ones are not being discovered. The lackluster performance of Pakistan's manufacturing sector in terms of exports illustrates this point.

The same lack of confidence in fundamentals underlies the low level of direct foreign investment as well. Unlike many countries in East Asia, Pakistan was unable to become a big part of the global production chains that became established over the past three decades. Now that globalization seems to be peaking, it is unlikely to get a foothold in the export of manufactures.

Now consider public investment. Why is public investment not at a higher level? This is because of the failure to generate adequate revenues from the domestic tax base. As long as the tax base remains as narrow as it is, and evasion, exemptions and avoidance remain high, public investment will continue to be constrained. As it is, public investment is highly dependent on the inflow of official loans from foreign donors.

Human Capital

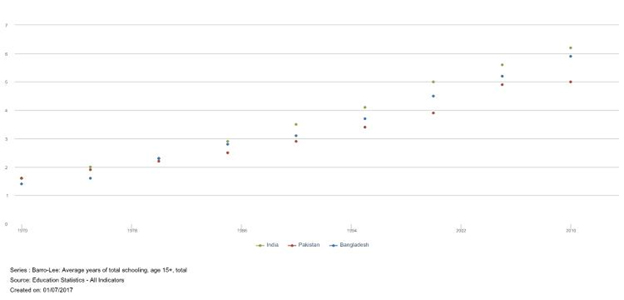

Let us now take a look at the other major determinant of growth. This is human capital. At one point, it was thought that rising education attainment among the population would be sufficient to generate adequate growth. Pakistan's human capital story, however, has been disappointing in several respects.

First, the rate of growth of educational attainment has been low. Improvements in literacy, primary school enrolment and secondary school enrolment have occurred at a very slow pace compared to what is needed for growth and compared to regional comparators.

Second, the quality of education has remained very poor. In the end, it is not the quantity of human capital that matters so much for growth as its quality. There is little growth or productivity benefit to be derived from churning out low quality graduates, whether from school or from colleges and universities.

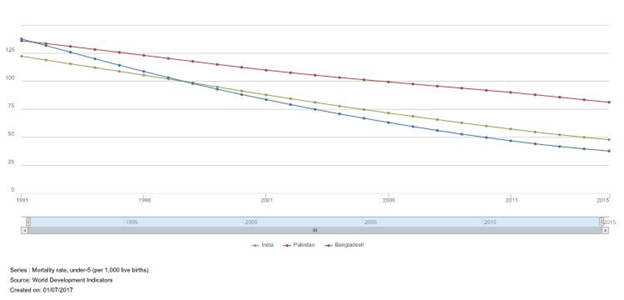

Human capital encompasses not just education but also health. Here as well, Pakistan's human capital story has been very disappointing. Indicators relating to the quality of health and access to health remain dismal. Pakistan has the third highest rate of stunting in the world; this refers to the height for age ratio among children under 5 years of age. Stunting affects brain development, cognitive ability, educability and health and through all these channels it affects productivity. Another prominent index of the quality of health and healthcare provision is the child mortality ratio. Pakistan's progress in this area has been slower than that of India and Bangladesh.

Human capital encompasses not just education but also health. Here as well, Pakistan's human capital story has been very disappointing. Indicators relating to the quality of health and access to health remain dismal. Pakistan has the third highest rate of stunting in the world; this refers to the height for age ratio among children under 5 years of age. Stunting affects brain development, cognitive ability, educability and health and through all these channels it affects productivity. Another prominent index of the quality of health and healthcare provision is the child mortality ratio. Pakistan's progress in this area has been slower than that of India and Bangladesh.

Institutions

There is a third determinant of long run growth which is best understood to refer to the institutional aspects of an economy or society, aspects such as corruption, transparency, rule of law, the burden of regulations, the extent of trust and social capital and so on. These aspects are independent of physical and human capital but affect the productivity with which such capital is applied.

There is a third determinant of long run growth which is best understood to refer to the institutional aspects of an economy or society, aspects such as corruption, transparency, rule of law, the burden of regulations, the extent of trust and social capital and so on. These aspects are independent of physical and human capital but affect the productivity with which such capital is applied.

Some institutional aspects have been partially quantified and their effects statistically studied. Such studies show that institutional quality does matter for long term economic growth and development.

The available data also show that Pakistan ranks poorly in institutional quality. It does not necessarily rank worse than many of its regional comparators but it does rank at the lower end of measures of corruption, rule of law, the burden of regulations on business and so on.

Long-run outcomes

What are the long run consequences of the deficiencies in physical capital formation, human capital formation and institutional quality that I have just identified above?

One long run consequence is that economic growth rates tend to be lower than potential. This is illustrated in the next graph for India and Pakistan. During the last quarter century or so, India's economic growth rates have been higher than those of Pakistan. There are many reasons for this but they surely include the fact that Pakistan's rates of physical and human capital formation have been lower than those of India.

In summary then, while several aspects of short term economic performance are encouraging, the status of various determinants of long run growth suggest that Pakistan has a long road to travel.